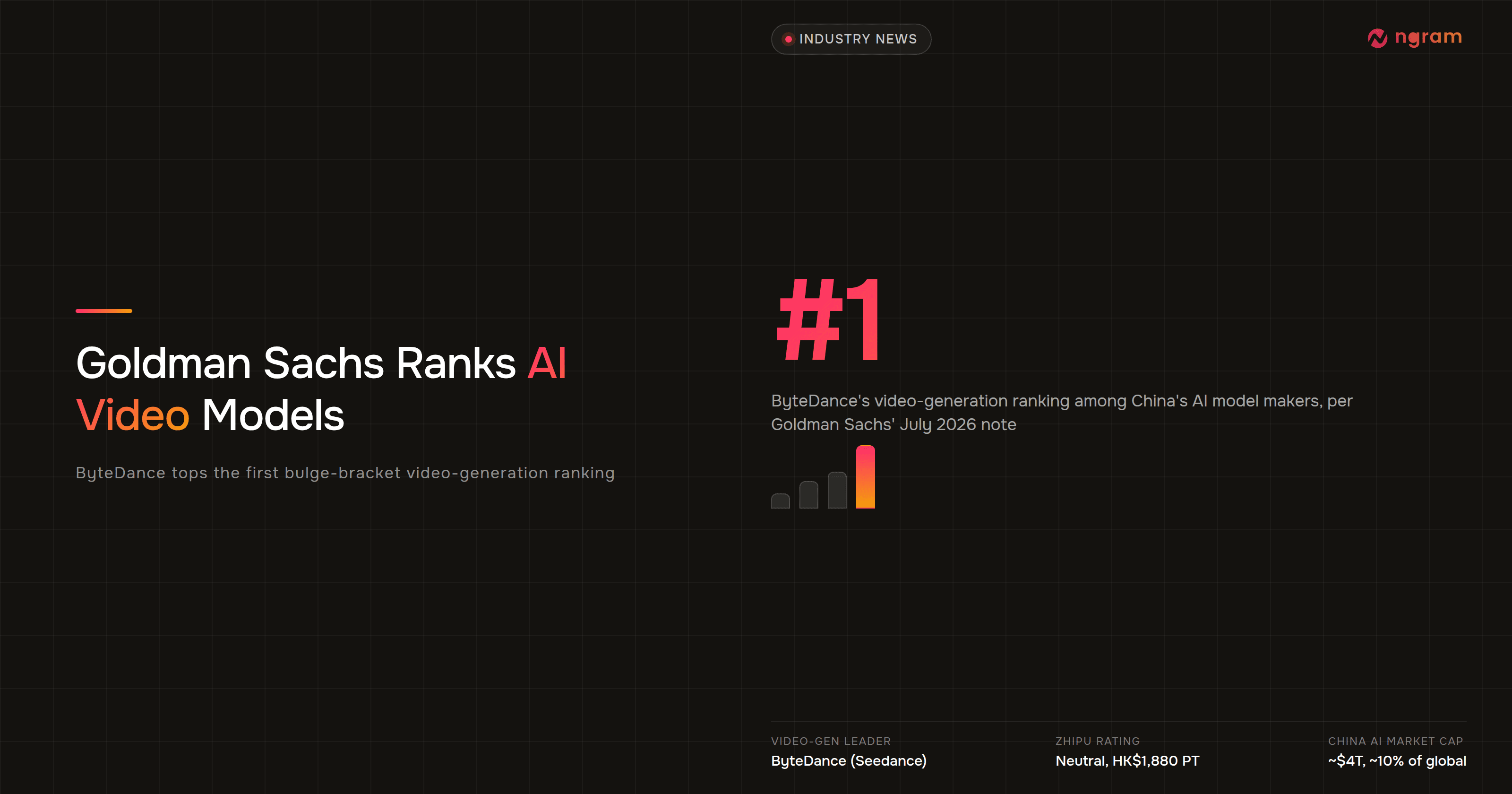

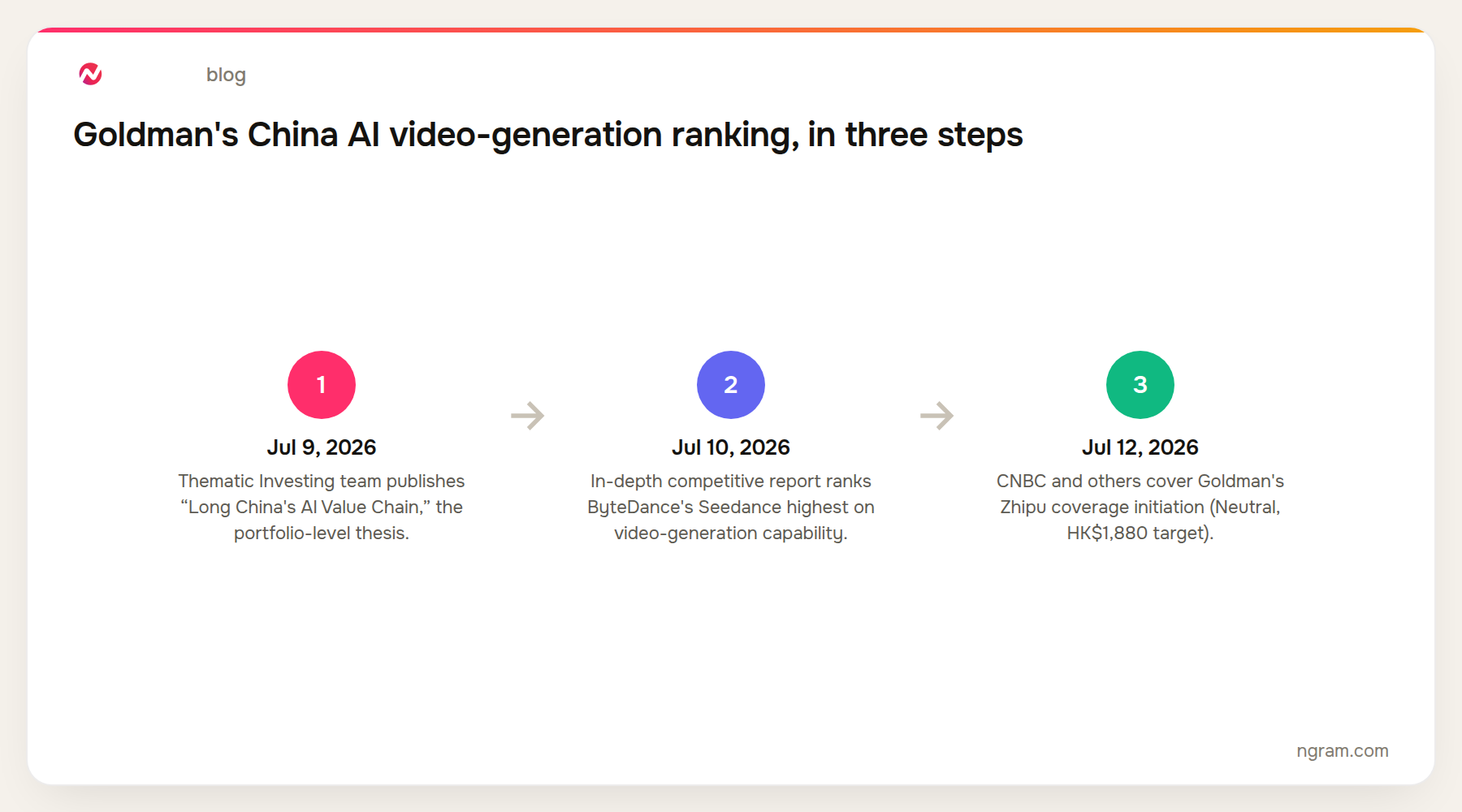

On July 9, 2026, Goldman Sachs' Thematic Investing team published a note titled “Investment Strategy: Long China's AI Value Chain,” telling clients to go long on Chinese AI stocks. Three days later, on July 12, the bank went further. It initiated coverage on Zhipu, the only one of its three preferred Chinese AI model makers that trades on a public exchange, and it ranked ByteDance's video-generation models, built on Seedance, above every other developer it evaluated, including Zhipu itself, per IBTimes.

That is not a detail buried on page 40 of a research note. It is the first time a bulge-bracket bank has published an investable ranking of AI video-generation quality as its own category, separate from chat and language-model benchmarks. Goldman scored Zhipu and DeepSeek highest on foundational text models. Then, in a section evaluated on different criteria, it ranked ByteDance's video-generation capability above Zhipu, DeepSeek, Alibaba, Tencent, and Minimax.

Read that as institutional capital telling the market, on letterhead, that video generation is a distinct competitive axis in the AI stack, separate from “how good is this model at everything.” It also lands three weeks after Alibaba joined a $2 billion-plus round for Kuaishou's Kling AI and eleven days after two Hollywood studios took equity stakes in AI video providers, both covered in detail below. Three separate capital events, one shared bet: the money now thinks real differentiation in AI lives in video generation, not general chat quality.

What Goldman Sachs actually said in its China AI note

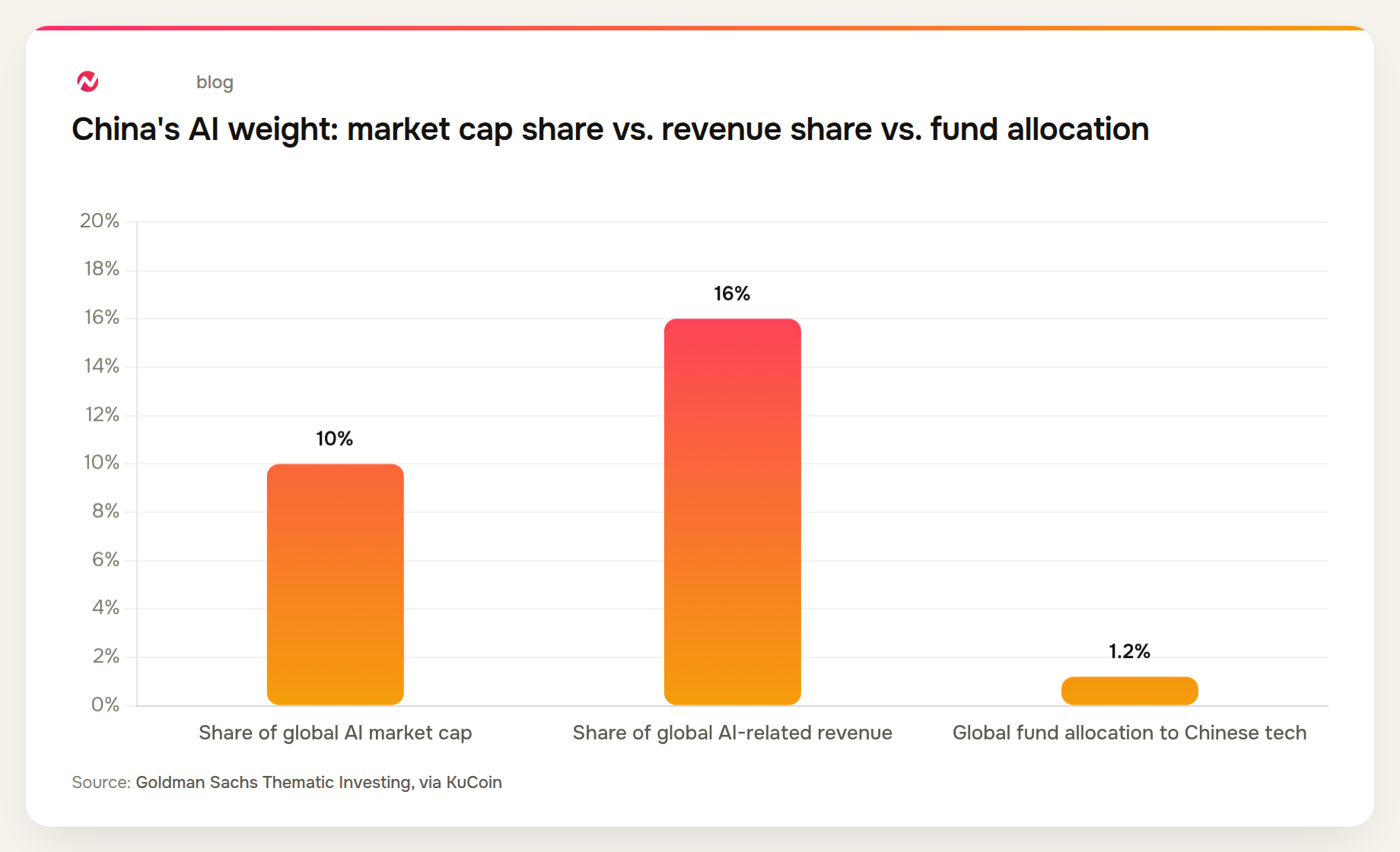

The July 9 note came from Goldman's Thematic Investing group and made a portfolio-level case: global AI-related public companies have added roughly $34 trillion in combined market capitalization since ChatGPT's late-2022 launch, but China's entire AI sector accounts for only about $4 trillion of that, or roughly 10% of the global AI market cap, despite China generating an estimated 16% of global AI-related revenue, according to KuCoin's summary of the report. Global mutual fund allocation to Chinese technology stood at just 1.2% as of January 2026. Goldman's framing was blunt: China's AI value chain is underweight relative to its own output, and the bank estimated the potential economic benefit of China's AI buildout could be 50% to 100% higher than current stock prices imply.

The market reacted immediately. The Hang Seng China Enterprises Index jumped as much as 4.5% intraday on the day the note went out, its largest single-day gain since February 2025, per the same KuCoin report. That reaction says the thesis wasn't a surprise so much as a confirmation of something capital was already leaning toward.

The video-generation ranking: how ByteDance beat Zhipu, DeepSeek, and everyone else

The video-generation ranking itself came from a separate, more granular piece of research: a roughly 50-page competitive deep-dive on China's AI large-model industry, led by Goldman analyst Ronald Keung, that CNBC and others covered on July 12 when Goldman initiated coverage on Zhipu. That deep-dive introduced a three-part scoring framework: pricing power (release speed, LMArena scores, price per million tokens), cost advantage (throughput, cache-hit rate, parameter-activation ratio, inference gross margin), and financial strength (cash reserves, net cash-to-assets ratio, valuation multiples).

On foundational text models, Zhipu and DeepSeek scored strongest, largely on pricing power and cost advantage. CNBC reported that Chinese high-end models run at roughly $1 per million tokens against $4 to $8 for comparable US models, and that Chinese architectures use 2% to 10% of the parameter counts of their US counterparts through mixture-of-experts routing. But on multimodal and video generation specifically, evaluated on time-to-market, Arena score, valuation, and pricing per Goldman's criteria, ByteDance's Seedance came out on top, ahead of Zhipu, DeepSeek, Alibaba, Tencent, and Minimax. Seedance and Kling are both text-to-video and image-to-video models at heart, and Kuaishou's Kling and Minimax's Hailuo and upcoming H3 model were also flagged positively for the second half of 2026 on expected video-generation and LLM-integration breakthroughs.

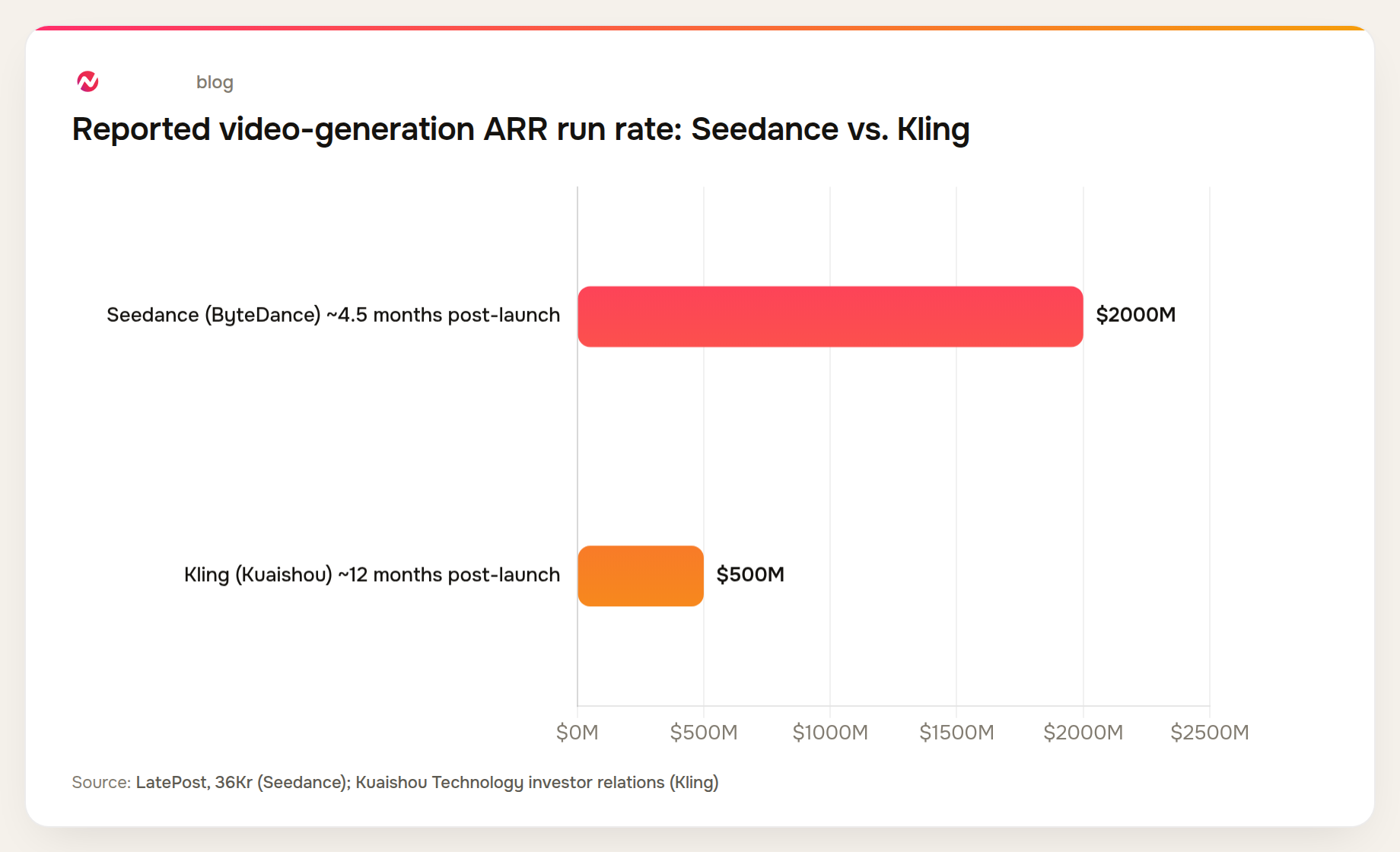

The number behind that ranking, cited by Chinese financial outlets LatePost and 36Kr, is the kind of figure that explains why Seedance specifically topped the list: an annualized revenue run rate reportedly exceeding $2 billion within roughly four and a half months of Seedance 2's launch, at a gross margin near 70%. Kuaishou's Kling, by comparison, took a full year to climb from $100 million to $500 million in annualized run rate, a slower ramp on a lower base, even though Kling has been public about its numbers longer and is the more mature business overall.

That comparison is not apples to apples. The two figures come from different sources, on different measurement windows, self-reported by companies with an obvious interest in looking strong. Treat it as a directional signal, not an audited number: video-generation businesses at the frontier are ramping revenue faster than the model layer's other, older cost centers, and that ramp is exactly what a research desk scoring “cost advantage” and “valuation” would reward.

Zhipu's coverage initiation: a Neutral rating on a stock that already ran 1,500%

Goldman initiated Zhipu, which trades as Knowledge Atlas Technology (2513.HK), at Neutral with a HK$1,880 price target, about 15% above where the stock closed the Friday the coverage went live. The analyst note, quoted by IBTimes, put it this way: “With its latest GLM-5.2 model reaching near-frontier performance that has seen significant ramp-up in domestic enterprise and global SME adoption, we believe its extensive usage by coders will enable Zhipu to sustain high frequency of further model upgrades.”

A Neutral rating undersells how far this stock had already run. Zhipu shares were up roughly 1,500% since the company's January 2026 Hong Kong listing by the time Goldman's note landed, according to Bloomberg. A day before Goldman's coverage note, on July 8, Zhipu priced a $4 billion follow-on share sale at HK$1,588 to HK$1,698 per share, a discount of up to 13% to its prior close, timed right after a six-month lockup on 25.68 million shares expired. Shares still jumped another 22% once the placement priced at the low end of that range, per a second Bloomberg report. Zhipu says the proceeds go toward compute infrastructure and continued model development, not balance-sheet padding.

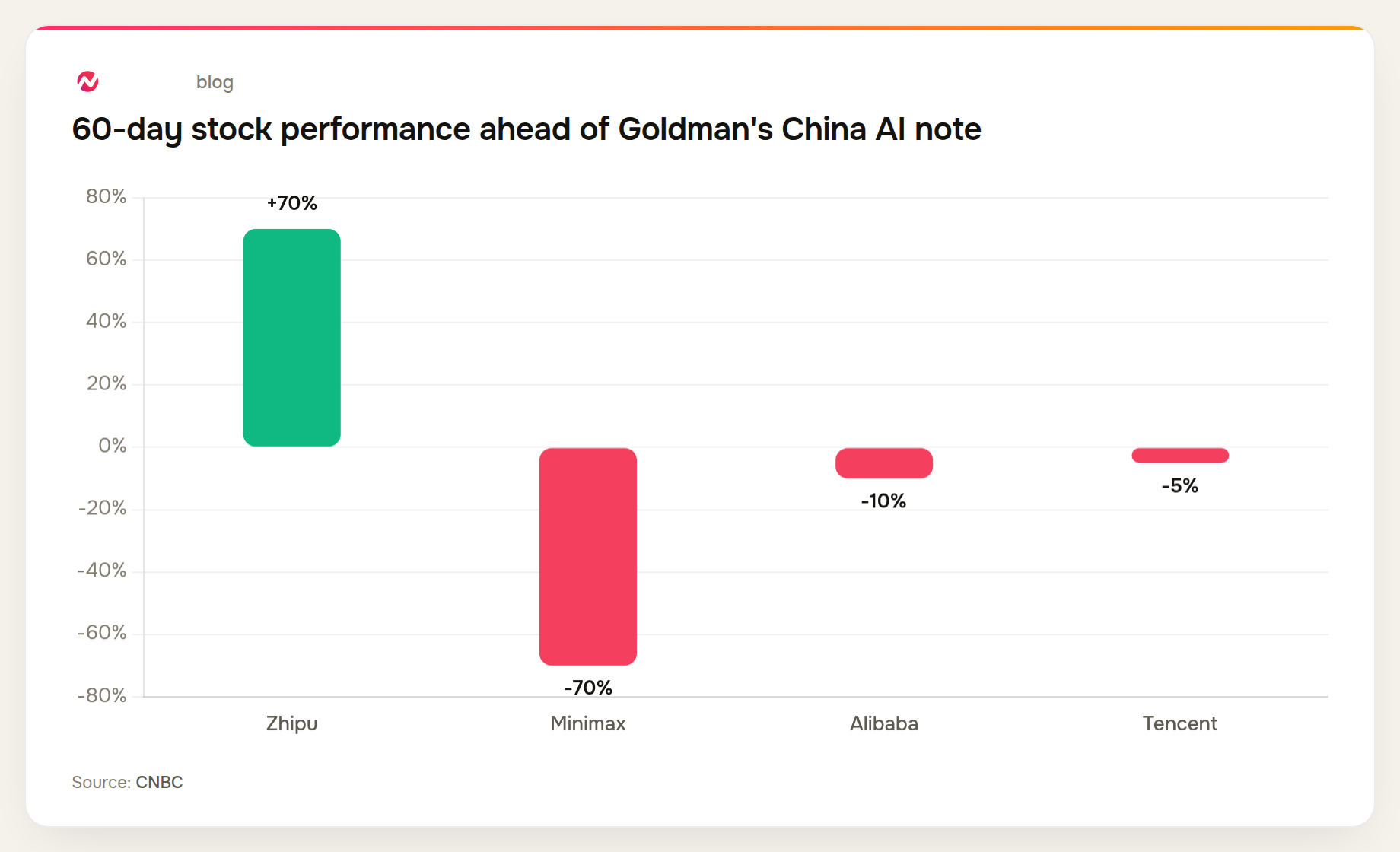

Over the 60 days leading into Goldman's note, the four Chinese AI-adjacent stocks it discussed moved in sharply different directions: Zhipu up 70%, Minimax down 70%, Alibaba down 10%, and Tencent down 5%, per CNBC's coverage. That spread is the market already doing, informally, what Goldman's note then did formally: pricing individual AI bets on their own merits rather than treating “Chinese AI” as one basket.

The third capital-markets-video moment in three weeks

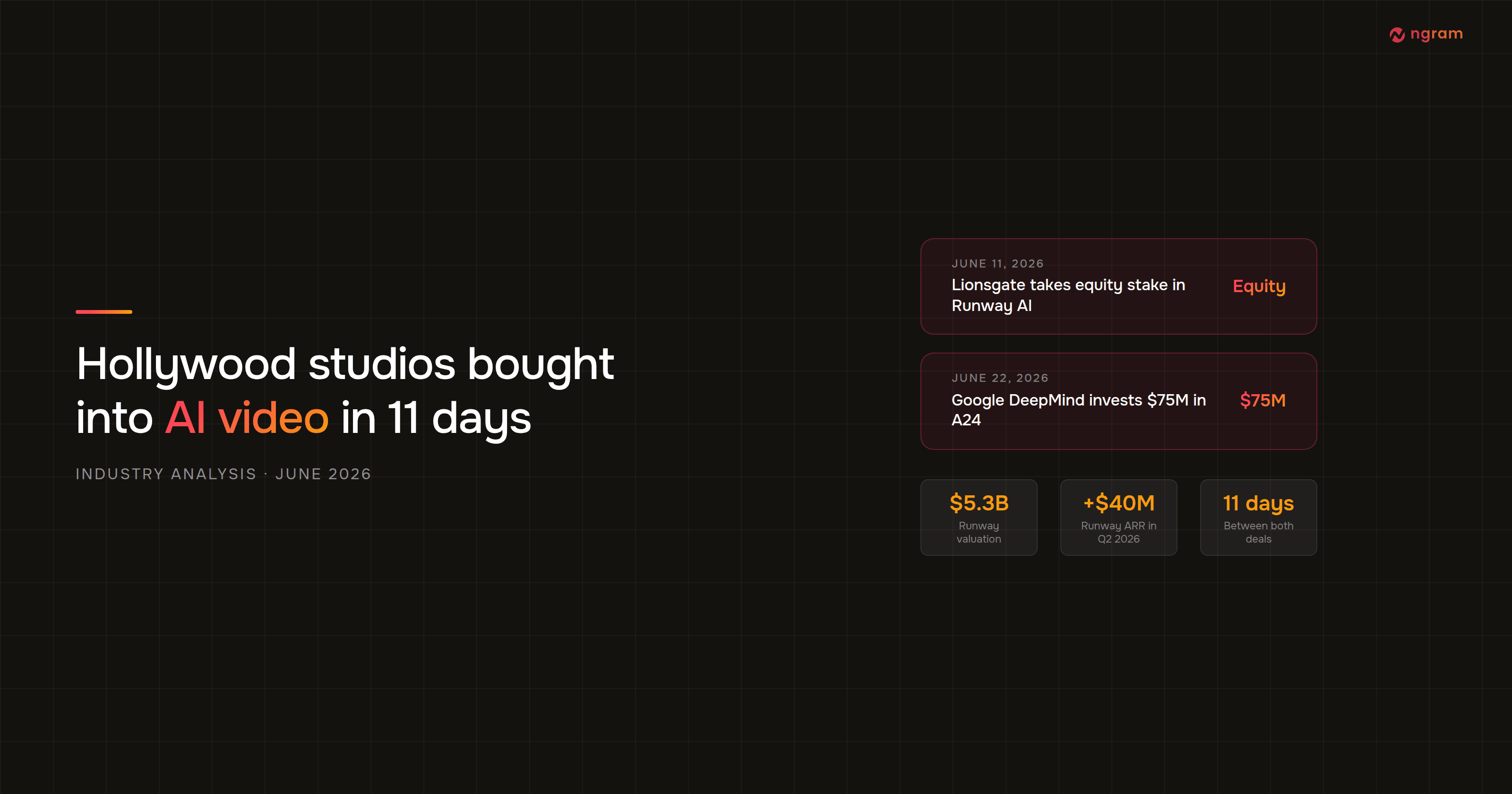

Line this note up against the calendar and a pattern shows up. On July 2, Kuaishou's Kling AI confirmed a funding round north of $2 billion at an ~$18 billion valuation, with Alibaba among the reported participants, ahead of a targeted 2027 Hong Kong IPO. In late June, within an 11-day window, A24 and Lionsgate each took equity stakes in AI video providers, neither framing the deal as cost-cutting. Now, on July 9 through 12, Goldman Sachs has done something different in kind from either of those: it published a formal, sell-side research ranking of video-generation quality, available to any institutional client, not tied to a single company's cap table.

A funding round is one investor's bet. An equity stake is one studio's bet. A bulge-bracket research ranking is a bank telling its entire client base how to think about a category. That is a meaningfully bigger vote of confidence than either private deal, and it is the first time this specific kind of vote has landed on video generation rather than chat.

Why capital is finally pricing video generation as its own signal

For most of the last three years, “AI quality” has meant one thing in public markets: how a model performs on chat and reasoning benchmarks. Video generation got funded, but mostly as a feature of a broader model story, not as a distinct axis institutional analysts bothered to score on its own criteria.

Goldman's framework breaks that habit on purpose. It scores foundational text models on one set of criteria and multimodal and video-generation models on a different, overlapping but distinct set, arriving at different leaders for each. Zhipu and DeepSeek win on text. ByteDance wins on video. That is the tell: the ai video generation platform layer now has its own economics, gross margin per generated clip, throughput per GPU-hour, time-to-market on a leaderboard specific to video, that don't move in lockstep with chat quality.

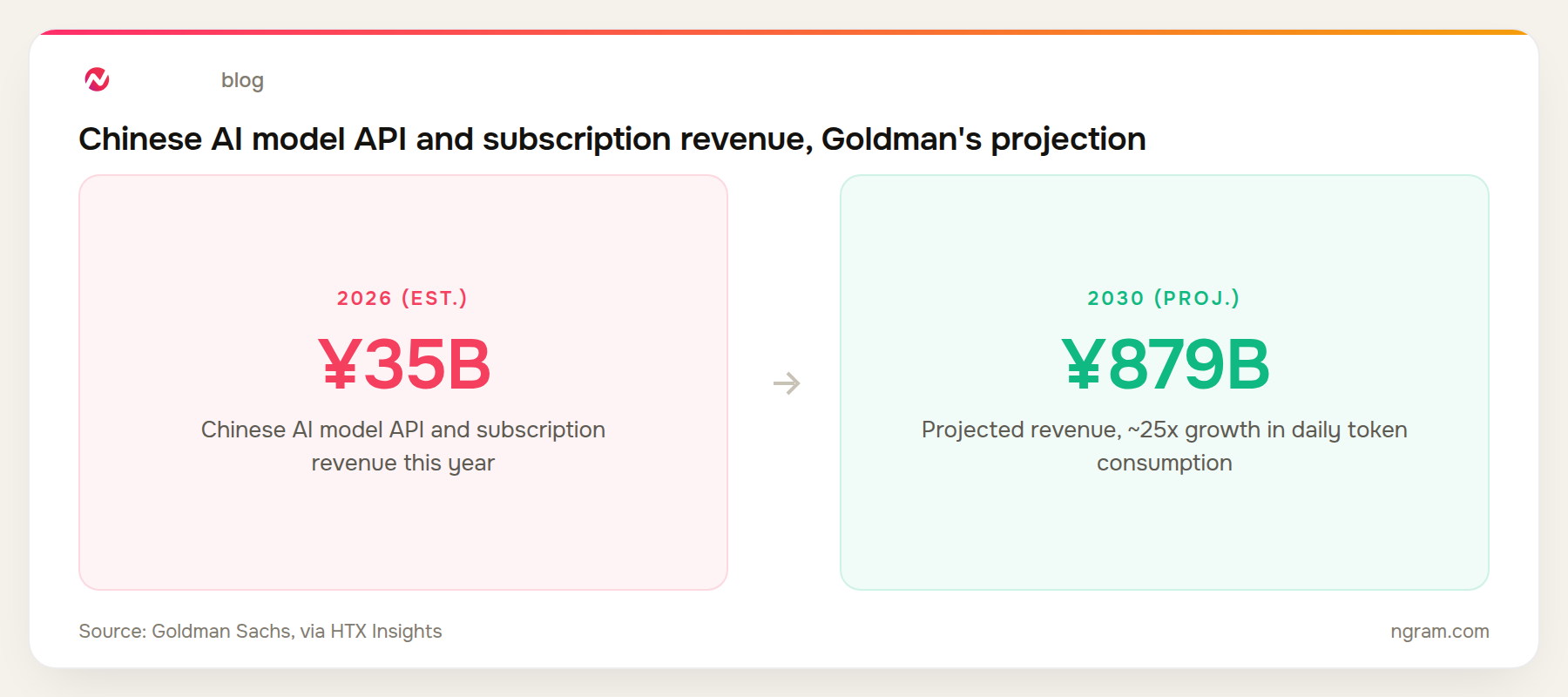

Goldman also projects that Chinese AI model API and subscription revenue will grow from an estimated 35 billion yuan in 2026 to 879 billion yuan by 2030, roughly a 25-fold increase in daily token consumption over four years. That is the demand curve the bank thinks justifies underwriting the model layer this aggressively, video generation included, even before any single company in it has gone public.

The wrinkle: ranked #1 on capability, still frozen on distribution

Here is what makes this ranking more interesting than a simple leaderboard. ByteDance froze Seedance 2.0's global rollout in March 2026 after Disney, Warner Bros., Paramount Skydance, Sony, Netflix, and the Motion Picture Association sent cease-and-desist letters over deepfake and copyright concerns, the first time the MPA had issued such a letter to an AI company. ByteDance responded by adding C2PA watermarking and content filters that block recognizable real faces and copyrighted characters, but as of this writing no formal litigation has been filed and the freeze on the model's broader international rollout has not been publicly lifted.

Four months later, Goldman ranked that same company's video-generation capability above every other Chinese model maker it evaluated. Capability and distribution risk are being priced as two separate variables here, not one combined reputation score. A model can be the best in its category on Arena and still carry real legal overhang in the markets that matter most commercially. That is a more sophisticated way to read the AI video space than either “ByteDance is unstoppable” or “ByteDance is legally radioactive,” and it is worth sitting with before treating this ranking as an uncomplicated endorsement.

What a formally-ranked video-generation layer means for teams building on top of it

Zoom out from the specific ranking and the signal for anyone building on ai video platforms, rather than training one, is straightforward: the layer you depend on is getting more capital, more scrutiny, and more competitive pressure to keep improving, all at once. A model vendor a bulge-bracket bank is now scoring on cost advantage and pricing power is a vendor under real pressure to keep shipping better, cheaper generation, not a side project someone can quietly deprioritize.

That is a tailwind for the product layer sitting above the model layer, the part of the stack that takes a prompt or a script and turns it into a finished, on-brand video regardless of which ai video generator happens to be winning this quarter's leaderboard. ngram's own planning layer, script generation, storyboard generation, scene-by-scene planning, and the video-type picker that drives AI motion graphics, avatar video, or screencast-plus-avatar output, sits above that generation layer rather than being built around any single vendor's model. If you want to see what that looks like end to end, ngram is free to start.

What to watch next

- Whether Kling, Veo, or Runway publish their own investor-grade video-generation metrics now that a bulge-bracket desk has shown it will score the category on cost advantage and time-to-market.

- Zhipu's next earnings print against Goldman's Neutral rating and HK$1,880 target, especially after the $4 billion follow-on placement diluted the stock right before coverage began.

- Whether other banks publish their own China AI competitive frameworks, and whether any of them adopt video generation as a standalone scoring category the way Goldman just did.

- Whether the Hollywood cease-and-desist letters against ByteDance escalate into formal litigation, or quietly resolve, either of which would change how investors price the capability Goldman just ranked first.

- Whether Chinese AI API and subscription revenue tracks anywhere near Goldman's 35-billion-to-879-billion-yuan 2026-2030 projection, or falls short of the 25-fold token-consumption growth that projection assumes.

Frequently Asked Questions

What did Goldman Sachs say about China's AI value chain?

On July 9, 2026, Goldman Sachs' Thematic Investing team published “Investment Strategy: Long China's AI Value Chain,” recommending clients go long on Chinese AI stocks. The note argued China's AI sector, at roughly $4 trillion in market cap, is undervalued relative to its 16% share of global AI-related revenue and the sector's broader growth prospects.

Why did Goldman Sachs rank ByteDance above Zhipu and DeepSeek on video generation?

Goldman scored Chinese AI developers on different criteria depending on category. On foundational text models, Zhipu and DeepSeek led on pricing power and cost advantage. On multimodal and video generation specifically, evaluated on time-to-market, Arena score, valuation, and pricing, ByteDance's Seedance ranked highest, ahead of Zhipu, DeepSeek, Alibaba, Tencent, and Minimax.

What rating and price target did Goldman Sachs give Zhipu?

Goldman initiated Zhipu (Knowledge Atlas Technology, 2513.HK) at Neutral with a HK$1,880 price target, about 15% above the stock's closing price the Friday coverage began. The rating landed one day after Zhipu priced a $4 billion follow-on share sale, and after the stock had already gained roughly 1,500% since its January 2026 Hong Kong listing.

How much revenue does ByteDance's Seedance generate?

Chinese financial outlets LatePost and 36Kr have reported Seedance's annualized revenue run rate exceeding $2 billion within about four and a half months of Seedance 2's launch, with a gross margin near 70%. Those figures are self-reported and not independently audited, so treat them as directional rather than precise.

Is this the first time a bank has ranked AI video-generation quality as investable?

It appears to be the first time a bulge-bracket bank has published a formal, standalone ranking of AI video-generation quality as its own investable category, distinct from chat and language-model benchmarks. Video-specific capital events have happened before, Kling's funding round and the Hollywood studio equity stakes among them, but those were private deals rather than sell-side research available to an entire client base.

How does this relate to Kling AI's funding round and the Hollywood AI-video equity deals?

All three events happened within about three weeks of each other in mid-2026 and point at the same underlying shift: capital treating video-generation quality as a distinct, valuable signal. Kling's ~$18 billion funding round and the A24 and Lionsgate equity stakes were company-specific and studio-specific bets. Goldman's ranking is different in kind: a bank-wide research framework any institutional client can act on.

Does ngram use ByteDance's Seedance models?

This report doesn't change what ngram ships today, and ngram doesn't publicly tie its product to any single underlying video-generation vendor. ngram's planning and production layer, script generation, storyboarding, scene planning, and its AI Motion Graphics, Avatar video, and Screencast-plus-Avatar output types, sits above that generation layer rather than being built around any one vendor's model. Which vendor powers a given generation is an internal implementation detail, not a claim ngram makes about itself.

Why is video generation being treated as separate from chat and LLM quality now?

Because the economics genuinely are separate. Video generation has its own cost structure (compute per generated second, gross margin per clip), its own leaderboards (Arena-style video benchmarks), and its own adoption curve, none of which move in lockstep with how good a model is at chat or reasoning. Goldman's decision to score them on different criteria and arrive at different category leaders is the clearest evidence yet that capital markets see the same split.