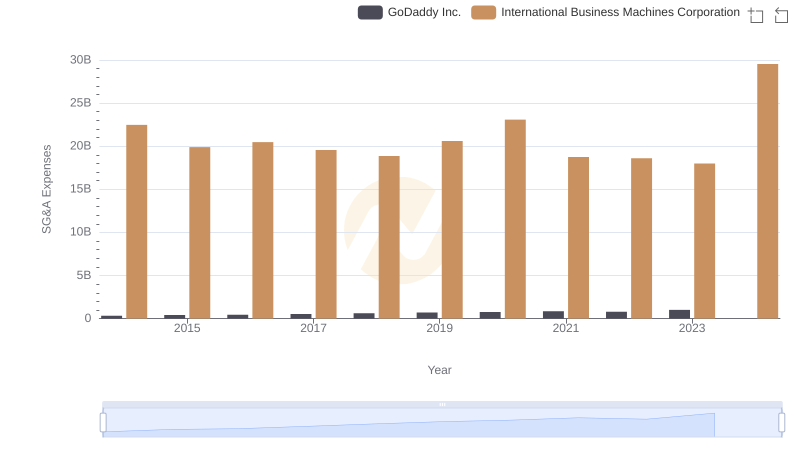

| __timestamp | GoDaddy Inc. | International Business Machines Corporation |

|---|---|---|

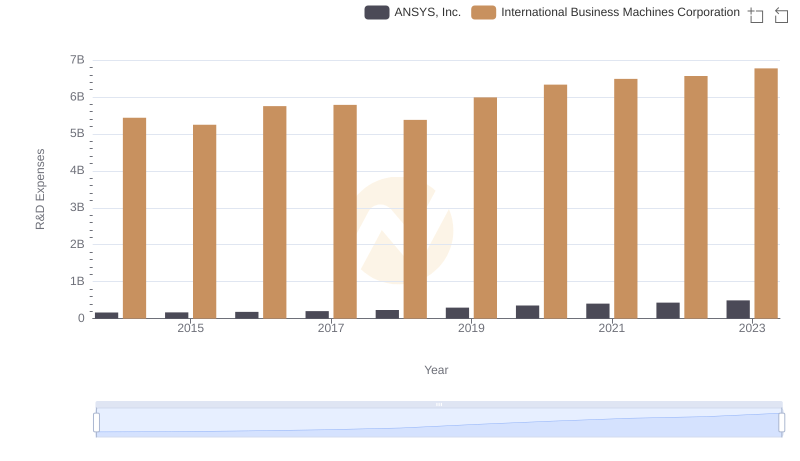

| Wednesday, January 1, 2014 | 254440000 | 5437000000 |

| Thursday, January 1, 2015 | 270200000 | 5247000000 |

| Friday, January 1, 2016 | 287800000 | 5726000000 |

| Sunday, January 1, 2017 | 355800000 | 5590000000 |

| Monday, January 1, 2018 | 434000000 | 5379000000 |

| Tuesday, January 1, 2019 | 492600000 | 5910000000 |

| Wednesday, January 1, 2020 | 560400000 | 6262000000 |

| Friday, January 1, 2021 | 706300000 | 6488000000 |

| Saturday, January 1, 2022 | 794000000 | 6567000000 |

| Sunday, January 1, 2023 | 839600000 | 6775000000 |

| Monday, January 1, 2024 | 814400000 | 0 |

Unleashing the power of data

In the ever-evolving landscape of technology, innovation is the key to staying ahead. This analysis delves into the research and development (R&D) spending trends of two tech giants: International Business Machines Corporation (IBM) and GoDaddy Inc., from 2014 to 2023.

IBM, a stalwart in the tech industry, has consistently prioritized R&D, with expenditures peaking at approximately $6.8 billion in 2023. Despite a slight dip in 2015, IBM's commitment to innovation remains unwavering, with an average annual R&D spend of around $5.4 billion over the decade.

GoDaddy, known for its web hosting services, has shown a remarkable upward trend in R&D investment, growing from $254 million in 2014 to $839 million in 2023. This represents a staggering 230% increase, underscoring GoDaddy's strategic focus on innovation to enhance its competitive edge.

While IBM's R&D spending dwarfs that of GoDaddy, the latter's rapid growth in investment highlights its ambition to innovate and expand its market presence. This comparison offers a glimpse into how these companies prioritize innovation to drive future success.

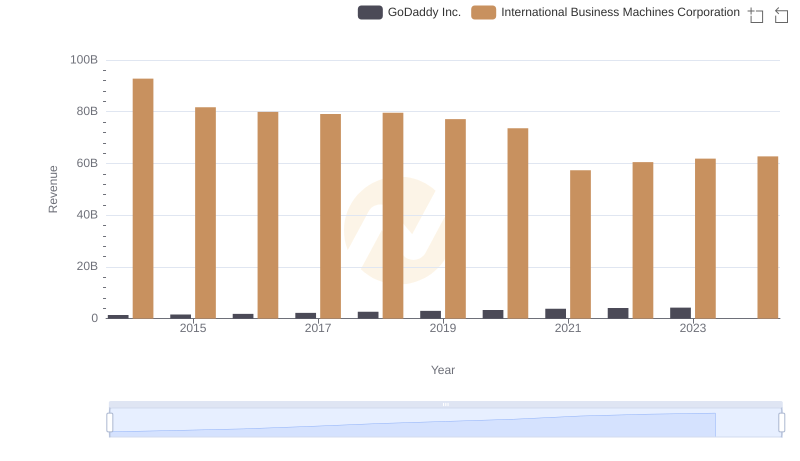

Who Generates More Revenue? International Business Machines Corporation or GoDaddy Inc.

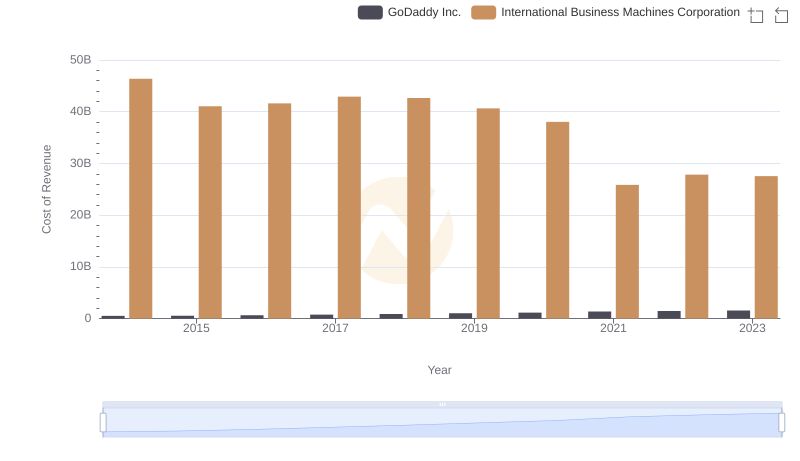

Cost Insights: Breaking Down International Business Machines Corporation and GoDaddy Inc.'s Expenses

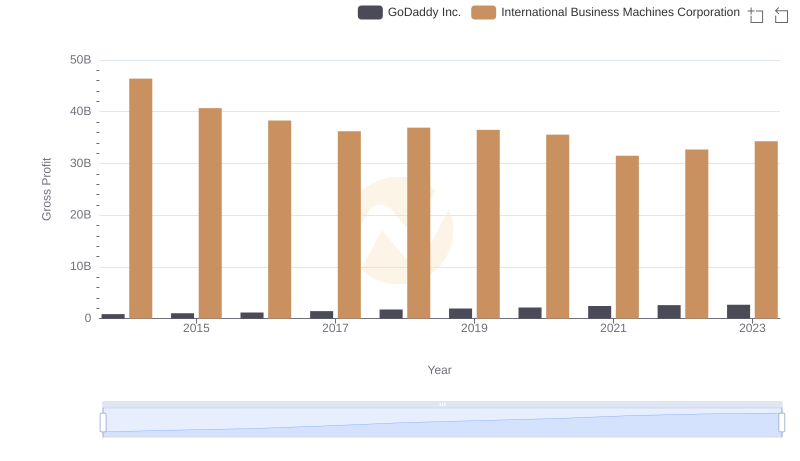

Gross Profit Comparison: International Business Machines Corporation and GoDaddy Inc. Trends

International Business Machines Corporation or ANSYS, Inc.: Who Invests More in Innovation?

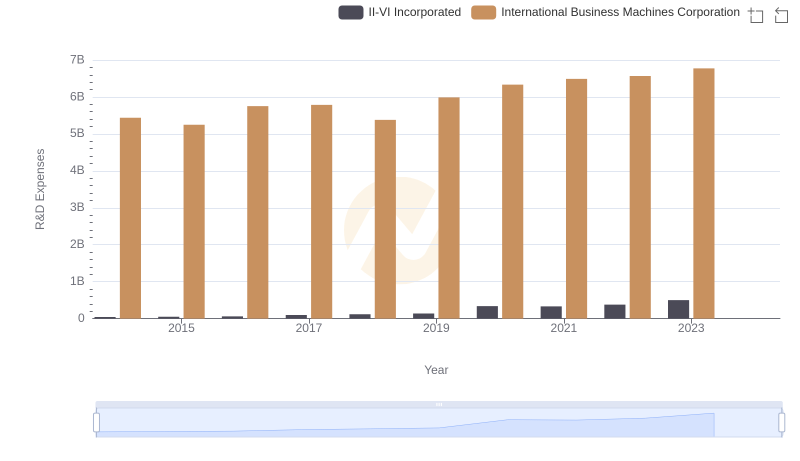

Research and Development Investment: International Business Machines Corporation vs II-VI Incorporated

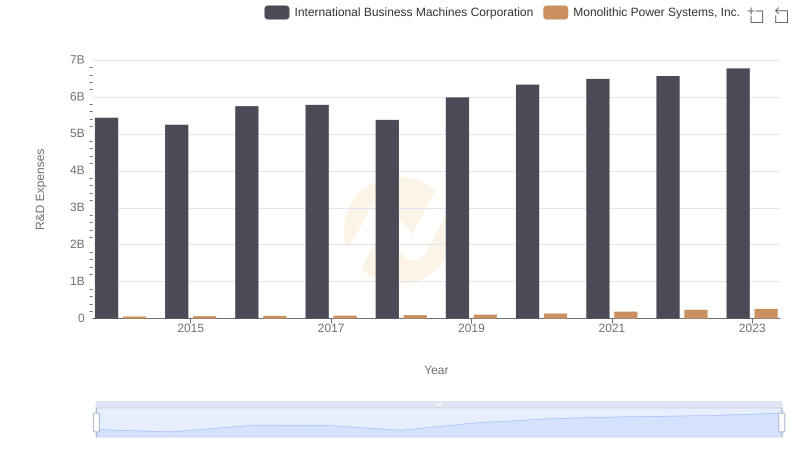

Research and Development: Comparing Key Metrics for International Business Machines Corporation and Monolithic Power Systems, Inc.

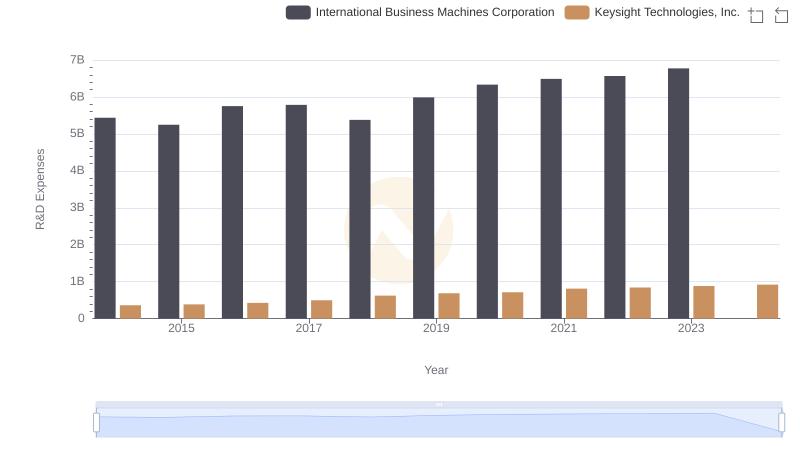

Research and Development Expenses Breakdown: International Business Machines Corporation vs Keysight Technologies, Inc.

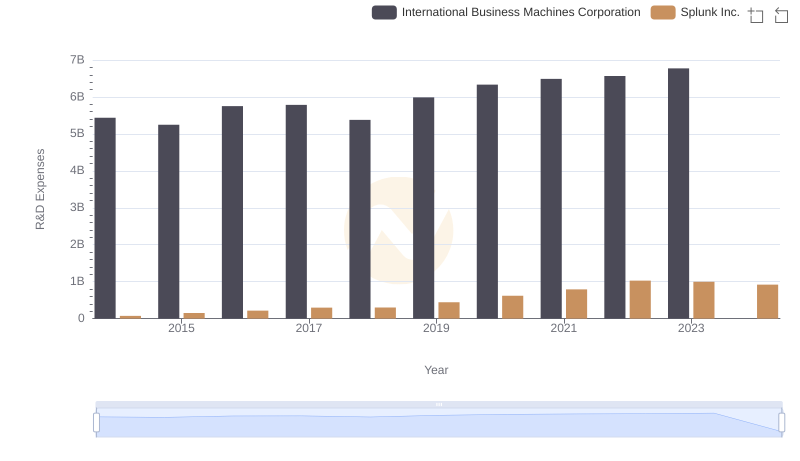

Comparing Innovation Spending: International Business Machines Corporation and Splunk Inc.

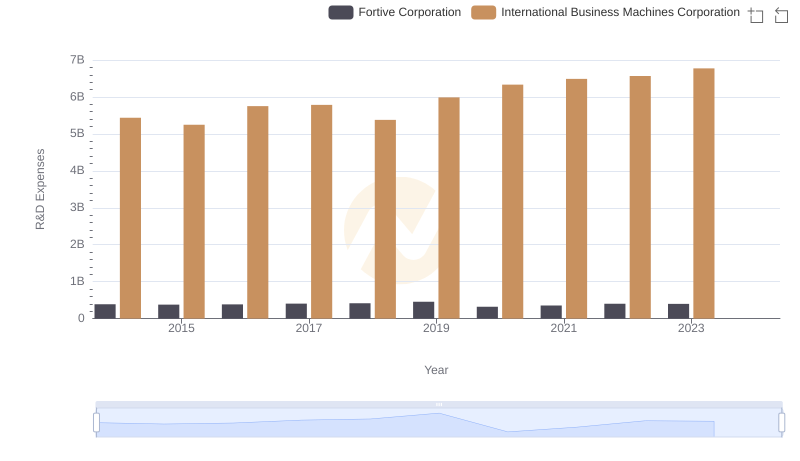

International Business Machines Corporation or Fortive Corporation: Who Invests More in Innovation?

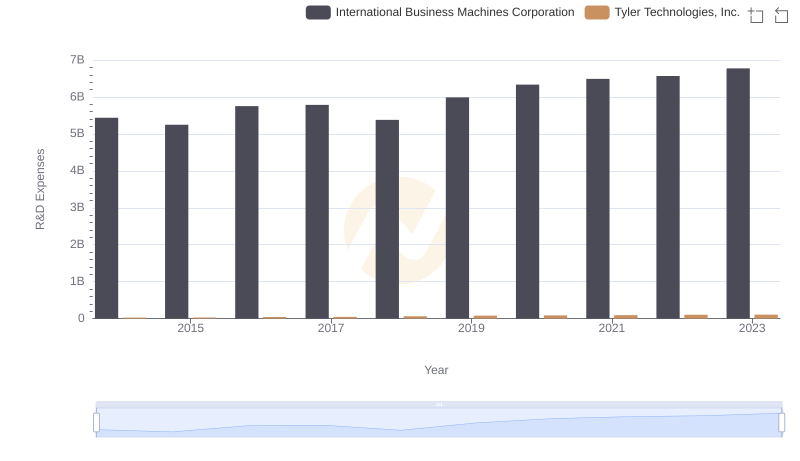

Research and Development Investment: International Business Machines Corporation vs Tyler Technologies, Inc.

Cost Management Insights: SG&A Expenses for International Business Machines Corporation and GoDaddy Inc.

Analyzing R&D Budgets: International Business Machines Corporation vs Telefonaktiebolaget LM Ericsson (publ)